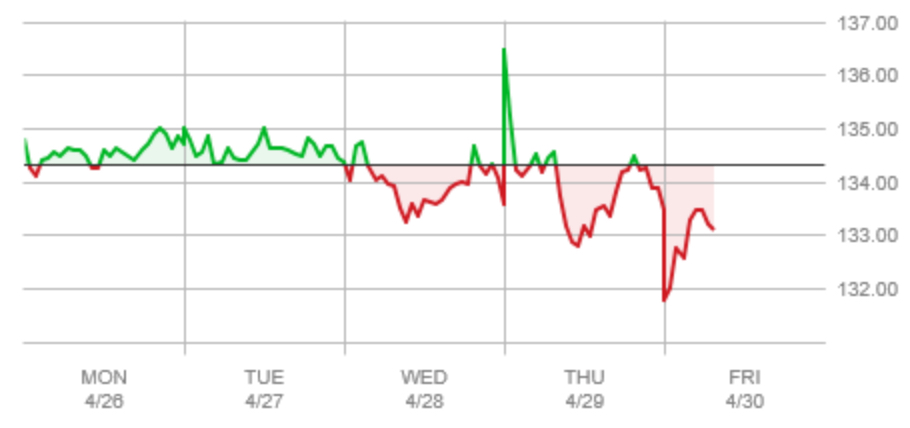

It is always interesting to observe blockbuster earning results (genuine fundamentals) and realize what is good for business, the economy, and employment, often has little or nothing to do with what drives the capital markets. In other words, what’s good for business is not necessarily good for stocks, and vice versa. Put another way still, investor and consumer confidence are two entirely different things, sometimes. Take just one example with Apple Computer and the 5-day price movement:

How does that reflect a company that just reported earnings that are on track to exceed last year by 30%? Additionally, Apple reported

Profit of $23.6 billion in the latest quarter as revenue rose 54% to $89.6 billion, far exceeding Wall Street expectations. The company also announced a 7% increase to its cash dividend to 22 cents a share and that the board had authorized an increase of $90 billion to an existing share-repurchase program (Ameritrade).

A similar assessment with the same question in Barron’s:

At least a dozen analysts raised their targets for the (AAPL) stock price…and every single one of them raised their earnings estimates in response to the results…previous (Goldman) view that iPhone sales would disappoint during the pandemic was “clearly wrong.”

…growth of 66% in iPhone sales, 70% for Macs, 79% for iPads, and 25% for Wearables, with 27% growth in Services. The company posted 56% growth in Europe, and a remarkable 88% in China…

One obvious question is what can Apple do as an encore?

The suggestion that the earning report might be a little “too good” kind of sound like a search something to say in the absence of any real explanation. But the question of what happens in post-pandemic consumer behavior is a valid one:

“Will there be a trough on the other side as Covid-driven wallet share shifts return to normal?”…“We think the answer is unequivocally yes. It’s just hard to know when and how big that trough might be. We believe that iPad and Mac strength could persist for the next two quarters, but even if the WFH trend persists, we doubt the surge will rival this year’s” (Barron’s).

So again, this week the positive news seems to continue the concern over what happens on the other side of pent up recovery and stimulus, as well as the threat of rising interest rates. But on the good for business and consumer side of things, it is noted, “Apple remains our top idea as we think the hardware business is still in the early parts of a multi-year growth cycle aided by product refreshes and work from home/hybrid work environments.”