By now, the study from the Brookings Institution, Is a Student Loan Crisis on the Horizon? has been gone over with a fine toothed comb. And the findings of the study are remarkable with a premise reflected by comments such as,

Typical borrowers are no worse off now than they were a generation ago, and [the data] also suggest that the borrowers struggling with high debt loads frequently featured in media coverage may not be part of a new or growing phenomenon. The percentage of borrowers with high payment-to-income ratios has not increased over the last 20 years—if anything, it has declined.

I think most people who read the above quote, whether in its context are not, have similar reactions. Namely, that this data simply does not, or cannot, square with a number of other variables that we know to be true regarding the pace of economic recovery for the last five years, employment, partial employment and unemployment, a growing variance in the income strata that is undeniable and leaving less and less in the middle, and a record low employment participation rate being among those in their twenties. But gut feeling, and anecdote do not prove anything, what about the data?

As a side note, I have come across a number of recent articles that have come out in a full-orbed, thoughtful response calling bunk on both data journalism, and the childlike faith whereby we accept astonishing correlations that we have never seen before, simply because they are backed up by data sets. I’m not saying there is not value and validity to statistics, but I do think our sociological infatuation with them in pop culture represents an innovation (in the bad sense) in need of some correction.

Dissenting Voices

There have been a number of dissenting voices, and one particularly effective one appeared on the Awl.com, That Big Study About How the Student Debt Nightmare Is in Your Head? It’s Garbage. The article treats volume of debt and rapidly rising tuition, but the ringer is this,

Do you see where that says “based on households with people between 20 to 40 years old with at least some education debt”?…Those aren’t households with people between 20 and 40; those are households headed by people between 20 and 40. Which is to say, this data excludes all people living in households headed by, say, their parents, or other adults.

Another commentary came from a very weighty source, Liberty Street Economics of the Federal Reserve Bank of New York,

We read with interest a new Brookings Institution report, Is a Student Loan Crisis on the Horizon?, assessing the weight of the student debt burden. It was also pleasing to see the New York Times, several of our Twitter followers, and others citing work on this blog in counterpoint.

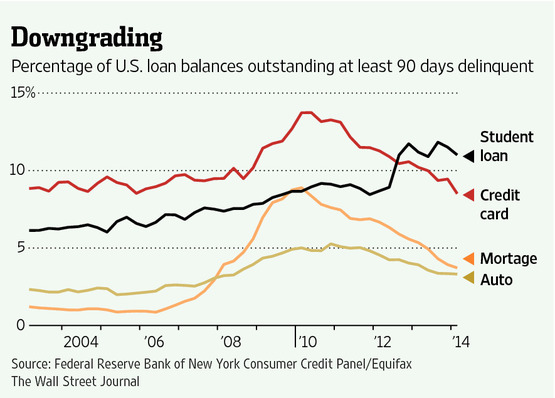

As part of our policy responsibilities at the New York Fed, we track the landscape of consumer credit, including student loans, using a unique data set developed here. A team of microeconomists described our approach in a March 2012 blog piece on “Grading Student Loans,” and reported key metrics such as the total outstanding student loan balance, averages balances per borrower by age group, and delinquencies at that time. Much of that data is updated quarterly here.

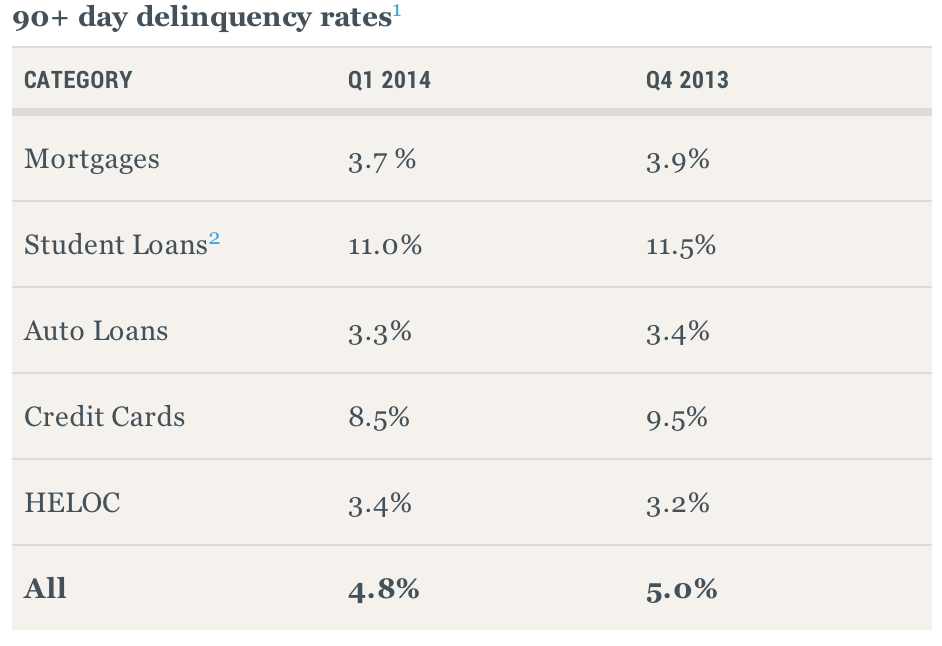

The New York Fed reports that among all other types of debt that increased in 1Q 2014, student loans weighed in with an increase of $31 billion. But most significantly, among the constellation of non performing assets, student loans topped the 90-day delinquency rate with a measurement of 11% – a full 2.5% above credit card delinquencies.

How are bankers reacting?

In The Wall Street Journal, an article titled, Bank Secrets Can Do Investors a Service revealed the following:

Banks have largely stopped making a very common type of loan. Investors should take note. In a recent paper titled “Banks As Secret Keepers,” four economists argue that banks are necessarily opaque institutions, concealing their portfolios and concentrating on hard-to-value assets. The reason: When investors and creditors can observe the performance of a bank’s assets too closely, its liabilities become volatile and illiquid. When bank assets are cloaked in secrecy, any given liabilities—deposits, repos, commercial paper—can be traded almost as if it were money.

Adding its own graphic on the subject with one notable item:

And here this the reason:

When investors and creditors can observe the performance of a bank’s assets too closely, its liabilities become volatile and illiquid. When bank assets are cloaked in secrecy, any given liabilities—deposits, repos, commercial paper—can be traded almost as if it were money.

Then this, “an exit often signals that the strategy wasn’t performing as well as hoped.” So what are the non performing assets that have bankers hitting the dump button? “Student lending. If the economists are right about the signaling aspect, this could be the next big troubled asset class for banks.”

As the article points out, even in a worst case scenario, no one expects troubled student loans to have the type comprehensive effects on our economy as the subprime mortgages. But if banking behavior as these institutions seek to mitigate risk is any kind of a leading indicator, all of the data available from the Fed does not seem alarmist at all.