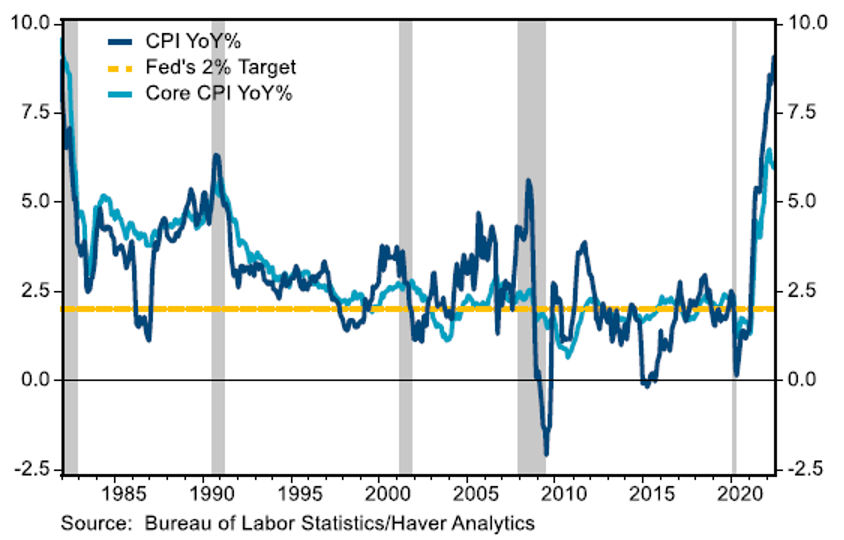

For years the monthly CPI report has been rather routine, with decades of low inflation and the challenge, from the perspective of the Fed, to target slightly higher, target inflation rates – something that sounds almost absurd in our present time. As always, there is a challenge on the part of the Federal Reserve to not overreact in one direction or another. The conundrum is more than two years of highly stimulative activity that followed more than a decade of stimulative activity. The discussion of how behind the Central Bank may be is an entirely different discussion. For now, it is a question of how much, how fast, and a very interesting question on the part of the markets regarding interpretation. Below is an excerpt from the Chief Economist at Stifel who presents a balanced and thoughtful assessment:

July CPI is expected to rise 0.2% and 8.7% over the past 12 months, according to Bloomberg data. Although, some including the Cleveland Fed anticipate a slightly higher read at 8.8%. In either case, this would be a welcome reprieve from a 9.1% near-term peak in June, although from a monetary policy perspective, may prove underwhelming. Committee members, after all, have been clear several months of a marked reduction in prices is needed before the Fed can comfortably say inflation is trending back under control. Therefore, one month’s minimal decline does not make a trend and should not have a material impact on the Committee’s latest hawkish rhetoric, or plans to move forward with a potential third-round 75bp hike in September.

…Investors, meanwhile, are still unconvinced of the Fed’s resolve to fight inflation no matter the costs with the 10-year restrained relative to a federal funds rate of 2.50% and a likely rise to 3.50% by year-end. As a result, expectations continue to ping pong between a 50bp or 75bp rise next month. A cooler-than-expected inflation report will likely tip the scale in the direction of a smaller move, while a hotter-than-expected report will all but solidify forecasts for 75bps.

Graphic source/credit: Stifel