Too big to fail is a narrowing option. And running with riskier assets is going to be costly for larger banking institutions, according to new rules by Federal Reserve as noted in the Wall Street Journal:

The Fed completed one rule stating that the eight largest banks in the country should maintain an additional layer of capital to protect against losses, its plainest effort yet to encourage them to shrink. At the same time, it offered a reprieve to General Electric Co.’s finance unit from more-intensive regulation, after the company promised to cut its assets by more than half.

…Regulators have pushed big banks to expand their capital buffers to better absorb losses, reduce their reliance on volatile forms of funding, improve their risk management and cut back on risky assets. So-called stress tests measure banks’ resilience each year and can restrict shareholder payouts at firms that don’t pass.

For Wall Street banks and their investors, the emerging regime presents a series of choices: specifically whether to pay the cost of new regulation, which will fall to the bottom line, or change their business models by shedding businesses or withdrawing from certain markets, such as owning commodities.

In a quote that I think is one of the best commentaries on the subject,

Fed Chairwoman Janet Yellen, before voting to approve the new measure, said financial firms must “bear the costs that their failure would impose on others.” She offered banks the choice of maintaining more capital to reduce the chance they would fail, or get smaller and reduce the harm their failure would have on the financial system.

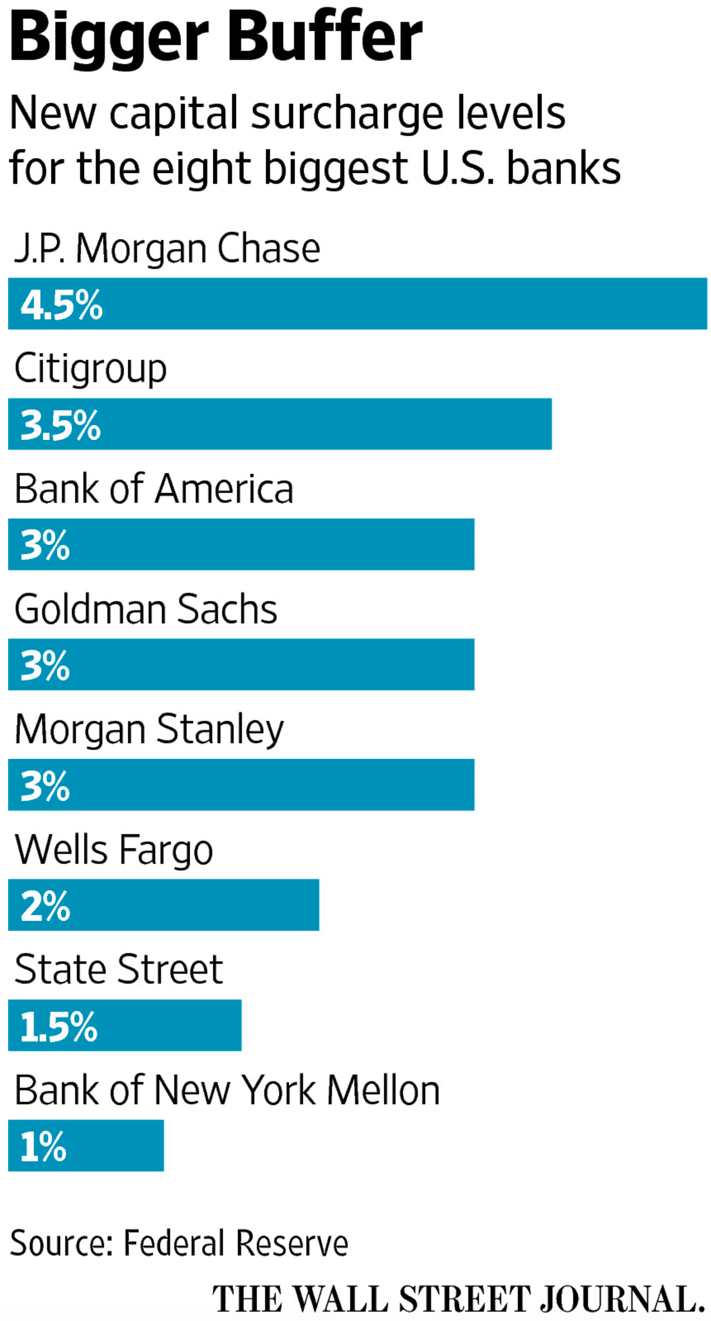

The big banks of course object to the action stating that it will remove billions from the economy. Below is a graph of the big 8 that will be hit with he most significant requirements (click for larger image):

But it is not size along that determines how each bank will be assessed, “the size of each bank’s additional capital requirement is tailored to the firm’s relative riskiness, as measured by the Fed’s formula, which considers factors such as size, entanglements with other firms and internal complexity. As those factors shrink or grow, so will a bank’s surcharge.”